Intuition

In the case of the IV, the confounding-fexaggeration trade-off is mediated by the ‘strength’ of the instrument considered. When the instrument only explains a limited portion of the variation in the explanatory variable, the IV can still be successful in avoiding confounders but power can low, potentially leading to exaggeration issues to arise.

Simulation framework

Illustrative example

To illustrate this loss in power, we could consider a large variety of settings, distribution of the parameters or parameter values. I narrow this down to an example setting, considering only one setting and one set of parameter values. I examine an analysis of the impact of voter turnout on election results, instrumenting voter turnout with rainfall on the day of the election. My point should stand in more general settings and the choice of values is mostly for illustration.

A threat of confounders often arises when analyzing the link between voter turnout and election results. To estimate such an effect causally, one can consider exogenous shocks to voter turnout such as rainfall. Some potential exclusion restriction problems have been highlighted in this instance Mellon (2021) but I abstract from them and simulate no exclusion restriction violations here.

Modeling choices

For simplicity, I make several assumptions:

- Observations are at the location level,

- Abstract from the panel dimension in this analysis and consider only one time period. This is could be considered as looking at the outcomes of a unique election,

- Only consider the impact of rain on the day of the election,

- Assume no correlation in rainfall between locations. This could be equivalent to considering only a set of remote locations,

- Assume simplify the data generating process and thus do not add any exclusion restriction violations.

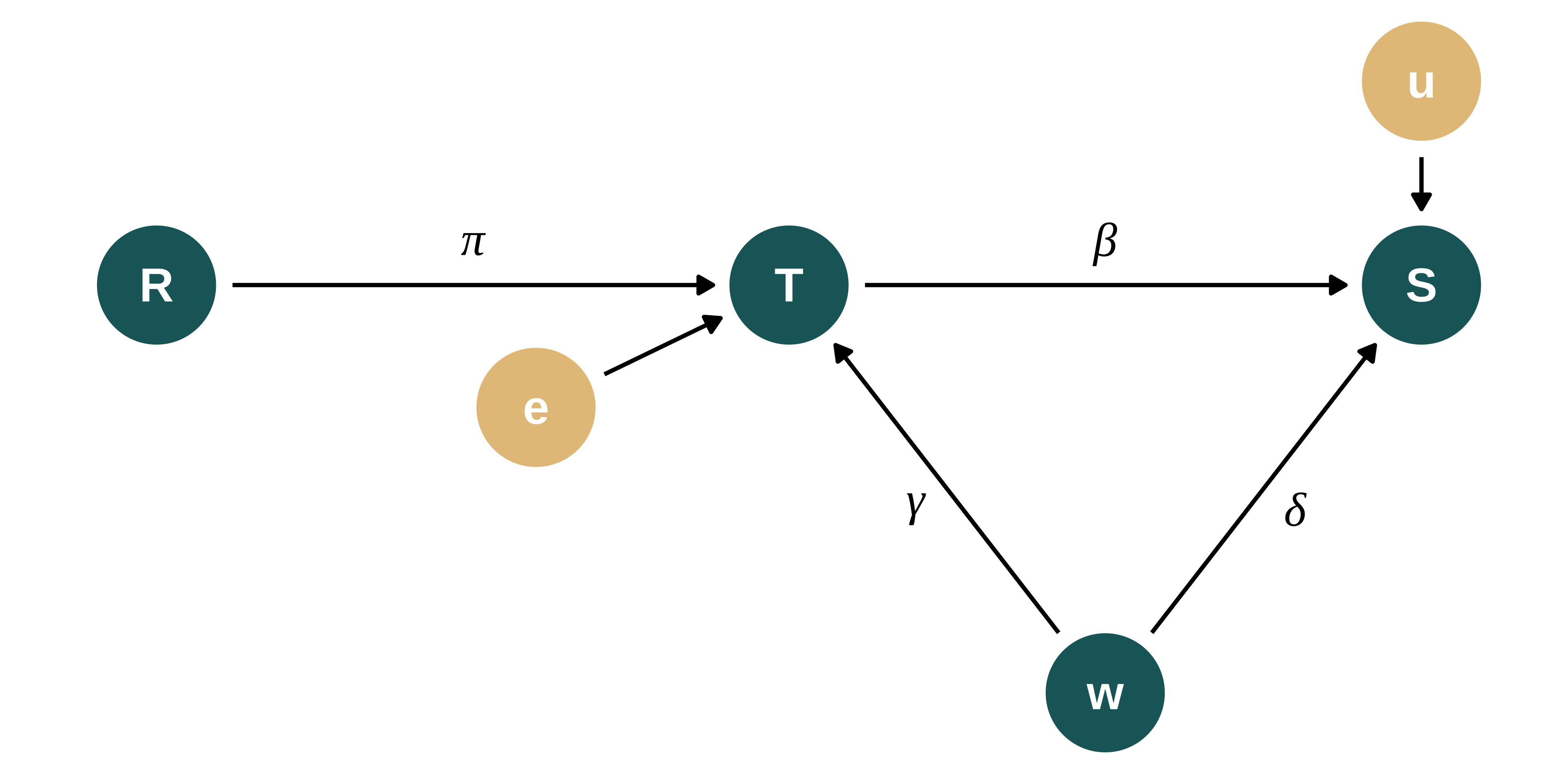

The DGP can be represented using the following Directed Acyclic Graph (DAG):

Show code

second_color <- str_sub(colors_mediocre[["four_colors"]], 10, 16)

dagify(S ~ T + w + u,

T ~ R + w + e,

exposure = c("S", "T", "R", "w"),

# outcome = "w",

latent = c("u", "e"),

coords = list(x = c(S = 3, T = 2, w = 2.5, R = 1, e = 1.6, u = 3),

y = c(S = 1, T = 1, w = 0, R = 1, e = 0.7, u = 1.5))

) |>

ggdag_status(text_size = 5) +

theme_dag_blank(legend.position = "none") +

scale_mediocre_d(pal = "coty") +

annotate(#parameters

"text",

x = c(2.5, 1.5, 2.8, 2.2),

y = c(1.1, 1.1, 0.45, 0.45),

label = c("beta", "pi", "delta", "gamma"),

parse = TRUE,

color = "black",

size = 5

)

The DGP for the vote share of let’s say the republican party in location \(i\), \(Share_i\), is defined as follows:

\[Share_{i} = \beta_{0} + \beta_{1} Turnout_{i} + \delta w_{i} + u_{i}\]

Where \(\beta_0\) is a constant, \(w\) represents an unobserved variable and \(u \sim \mathcal{N}(0, \sigma_{u}^{2})\) noise. \(\beta_1\) is the parameter of interest. Let’s call it ‘treatment effect’. Note that parameters names are consistent with the maths section and the other simulation exercises.

The DGP for the turnout data is as follows:

\[Turnout_{i} = \pi_0 + \pi_1 Rain_{i} + \gamma w_{i} + e_{i}\]

Where \(\pi_0\) is a constant, \(Rain\) is either a continuous variable (amount of rain in location \(i\) on the day of the election) or a dummy variable (whether it rained or not) and \(e \sim \mathcal{N}(0, \sigma_{e}^{2})\) noise. Let’s refer to \(\pi_1\) as “IV strength”.

The impact of voter turnout on election outcome (share of the republican party) is estimated using 2 Stages Least Squares.

More precisely, let’s set:

- \(N\) the number of observations

- \(Rain \sim \text{Gamma}(k, \theta)\), \(Rain \sim \mathcal{N}(0, \sigma_{R}^{2})\) or \(Rain \sim \text{Bernoulli}(p_R)\) the instrument

- \(w \sim \mathcal{N}(0, \sigma_{w}^{2})\) the unobserved variable

- \(u \sim \mathcal{N}(0, \sigma_{u}^{2})\)

- \(e \sim \mathcal{N}(0, \sigma_{e}^{2})\) with \(\sigma_{e}^{2}\) depending on \(\pi_1\) and defined such that \(\sigma_{Turnout}^{2}\) does not vary when we vary \(\pi_1\): \(\sigma_{e}^{2} = \sigma_{Turnout}^{2} - \pi_1^{2} \sigma_{Rain}^2 - \gamma^2\sigma_w^2\)

If one abstracts from the name of the variables, they can notice that this setting is actually very general.

Data generation

Generating function

Let’s first write a simple function that generates the data. It takes as input the values of the different parameters and returns a data frame containing all the variables for this analysis.

The parameter type_rain describes whether \(Rain\) is a random sample from a normal or Bernoulli distribution. The distributions of rainfall heights can be approximated with a gamma distribution. The Bernoulli distribution is used if one only consider the impact of rain or no rain on voter turnout. A normal distribution does not represent actual rainfall distributions but is added to run these simulations in other contexts than linking rainfall, voter turnout and election outcomes.

type_rain can take the values gamma, bernoulli or normal. param_rain represents either \(\sigma_R\) if \(Rain\) is normal, \(p_R\) if it is Bernoulli or a vector of shape and scale parameters for the gamma distribution.

generate_data_iv <- function(N,

type_rain, #"gamma", "normal" or "bernoulli"

param_rain,

sigma_w,

sigma_share,

sigma_turnout,

beta_0,

beta_1,

pi_0,

pi_1,

delta,

gamma) {

if (type_rain == "bernoulli") {

rain_gen <- rbinom(N, 1, param_rain[1])

sd_rain <- sqrt(param_rain[1]*(1-param_rain[1]))

} else if (type_rain == "normal") {

rain_gen <- rnorm(N, 0, param_rain[1])

} else if (type_rain == "gamma") {

rain_gen <- rgamma(N, shape = param_rain[1], scale = param_rain[2])

sd_rain <- sqrt(param_rain[1]*param_rain[2]^2)

} else {

stop("type_rain must be either 'bernoulli', 'gamma' or 'normal'")

}

data <- tibble(id = 1:N) |>

mutate(

rain = rain_gen,

w = rnorm(N, 0, sigma_w),

sigma_rain = sd_rain,

sigma_e = sqrt(sigma_turnout^2 - pi_1^2*sigma_rain^2 - gamma^2*sigma_w^2),

e = rnorm(N, 0, sigma_e),

turnout = pi_0 + pi_1*rain + gamma*w + e,

sigma_u = sqrt(

sigma_share^2

- beta_1^2*sigma_turnout^2

- delta^2*sigma_w^2

- 2*beta_1*delta*gamma*sigma_w^2

),

u = rnorm(N, 0, sigma_u),

share = beta_0 + beta_1*turnout + delta*w + u

)

return(data)

}Calibration and baseline parameters’ values

I now set baseline values for the parameters to emulate a somehow realistic observational study. I get “inspiration” for the values of parameters from Fujiwara, Meng, and Vogl (2016) and Cooperman (2017) who replicates a work by Gomez, Hansford, and Krause (2007).

I consider that:

- Number of observations: I consider data at the US county level as in Hansford and Gomez (2010) and Fujiwara, Meng, and Vogl (2016). The former use data for presidential elections between 1948 and 2000, restricting their sample of counties to non-Southern ones (2000 per election year). That leads to a sample size of 28000. The latter uses data for presidential elections between 1952 and 2012 leading to a sample size of about 50000. I thus consider 30000 observations.

- Rainfall distribution: A gamma distribution represents well the distribution of rainfall. Gamma distribution can have two parameters a shape and a scale. The mean is \(shape \times scale\) and the variance \(shape \times scale^{2}\). The parameters of the distribution of rainfall are comparable in both Fujiwara, Meng, and Vogl (2016) and Cooperman (2017) after a conversion into millimeters: mean 2.4 and standard deviation 6.6. I solve the system of mean and variance for shape and scale and set param_rain to 0.13 and 18. Following the literature, I only consider a continuous measure of rainfall.

- Effect of rainfall on turnout: Fujiwara, Meng, and Vogl (2016) find that “The trends specifications suggest that 1 millimeter of rainfall decreases turnout by 0.05–0.07 percentage points” and Gomez, Hansford, and Krause (2007) (and thus Cooperman (2017)) find “a county that receives one inch of rainfall on election day is likely to have approximately 1 percentage point lower voter turnout” which is equivalent to a 1mm difference in rainfall is associated with about a -0.04 percentage points difference in voter turnout. For simplicity in interpretation, when rainfall is not a dummy, I express it in millimeters. So, I consider pi_1 in the range -0.04 and -0.2, assuming linearity.

- Turnout and vote share are expressed in percent. I set intercepts and residual standard deviations to produce turnouts and vote shares consistent with Cooperman (2017) and Fujiwara, Meng, and Vogl (2016). Voter turnout parameters are roughly similar in both papers (mean 58 sd 14). The mean and standard deviation of Republican vote share are given in Fujiwara, Meng, and Vogl (2016) (mean 55.3 and sd 14.2). Thus, I set sigma_share = 14.2 and sigma_turnout = 14. pi_0 and beta_0 are manually adjusted to get the correct mean of turnout and vote share (for pi_1 in the mid-range of its values)

- Effect of interest (turnout on vote share): it is subject to intense debate in the literature (cf Shaw and Petrocik (2020) for instance). As underlined by Shaw and Petrocik (2020) and in Fowler (2013), some studies find large effects, others no effects or small effects. Fowler (2013) falls into the large effects category as described by the author himself (Fowler 2015). The study, for an extremely large shock in voter turnout, compulsory voting, finds “that the policy increased voter turnout by 24 percentage points which in turn increased the vote shares and seat shares of the Labor Party by 7 to 10 percentage points.” This correspond to a decrease in Republican vote share of approximately 0.3-0.4 percentage point when turnout increases by 1% (considering that this result is causal and linear). Fujiwara, Meng, and Vogl (2016) find “turnout falling 0.063 and 0.058 percentage points per millimeter of contemporaneous and lagged rainfall, respectively”. I choose an effect size between these two magnitudes: I simulate that when turnout increases by 1%, Republican vote share decreases by 0.2 and thus beta_1 = -0.2

- Effect of the omitted variable. The effect of the omitted variable cannot be observed, I consider that “income” as the omitted variable and assume that the identification strategy is not able to account for that. I compute a normalized version of the log income based on the data in Gomez, Hansford, and Krause (2007), after partialling out year to year variation, since I do not model any temporal dimension in my analysis. I define the correlation between this omitted variable and turnout and vote share by regressing both variable of log income and year fixed effects. For clarity, I further assume that \(\delta\) is negative to get an upward bias, which makes the comparison between OLS and IV easier since the bias and the exaggeration go in the same direction. If they don’t, exaggeration cancels OVB. In addition, one can relate this assumption to actual patters as in recent elections years, the correlation between Republican vote share and income became negative (yet the magnitude might be different).

Code to compute distribution OVB

# I retrieve data for Gomez from here:

#https://myweb.fsu.edu/bgomez/research.html

library(readr)

gomez <- read_csv(here("inputs", "IV_vote", "Weather_publicfile.csv")) |>

janitor::clean_names() |>

mutate(log_income = log(adj_income))

#delta

feols(gop_vote_share ~ log_income | year, data = gomez)

#gamma

feols(turnout ~ log_income | year, data = gomez)

#sigma_w

feols(log_income ~ 1 | year, data = gomez) |> resid() |> sd()

sd(gomez$log_income, na.rm = TRUE) Let’s thus consider the following parameters:

Show the code used to generate the table

baseline_param_iv <- tibble(

N = 30000,

# type_rain = "bernoulli",

# param_rain = 0.3,

type_rain = "gamma",

param_rain = list(c(0.13, 18)),

sigma_w = 0.28,

sigma_share = 14.2,

sigma_turnout = 14,

beta_0 = 60,

beta_1 = -0.2,

pi_0 = 59,

pi_1 = -0.05,

delta = -13.4,

gamma = 14.7

)

baseline_param_iv |> kable()| N | type_rain | param_rain | sigma_w | sigma_share | sigma_turnout | beta_0 | beta_1 | pi_0 | pi_1 | delta | gamma |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 30000 | gamma | 0.13, 18.00 | 0.28 | 14.2 | 14 | 60 | -0.2 | 59 | -0.05 | -13.4 | 14.7 |

Here is an example of data created with this data generating process:

Show the code used to generate the table

| id | rain | w | sigma_rain | sigma_e | e | turnout | sigma_u | u | share |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.0000003 | -0.1643113 | 6.489992 | 13.37734 | -19.446284 | 37.13834 | 13.17366 | -9.6955121 | 45.07859 |

| 2 | 0.0043522 | -0.2211127 | 6.489992 | 13.37734 | -10.655240 | 45.09419 | 13.17366 | 4.5245275 | 58.46860 |

| 3 | 0.0000000 | 0.4500603 | 6.489992 | 13.37734 | -4.925928 | 60.68996 | 13.17366 | 7.3605116 | 49.19171 |

| 4 | 4.7328542 | -0.1974975 | 6.489992 | 13.37734 | 5.971075 | 61.83122 | 13.17366 | -4.7516850 | 45.52854 |

| 5 | 0.0000863 | -0.0082812 | 6.489992 | 13.37734 | 8.021376 | 66.89964 | 13.17366 | 3.2696067 | 50.00065 |

| 6 | 0.0015507 | -0.1085520 | 6.489992 | 13.37734 | -14.067633 | 43.33657 | 13.17366 | -16.1009148 | 36.68637 |

| 7 | 0.4799312 | -0.4280953 | 6.489992 | 13.37734 | 21.885920 | 74.56892 | 13.17366 | 0.9802753 | 51.80297 |

| 8 | 0.0502115 | -0.1862775 | 6.489992 | 13.37734 | 4.311583 | 60.57079 | 13.17366 | 5.7308737 | 56.11283 |

| 9 | 0.0790413 | -0.0414453 | 6.489992 | 13.37734 | 8.452267 | 66.83907 | 13.17366 | -10.1846131 | 37.00294 |

| 10 | 0.0009223 | 0.1919409 | 6.489992 | 13.37734 | 2.604034 | 64.42552 | 13.17366 | -14.5344265 | 30.00846 |

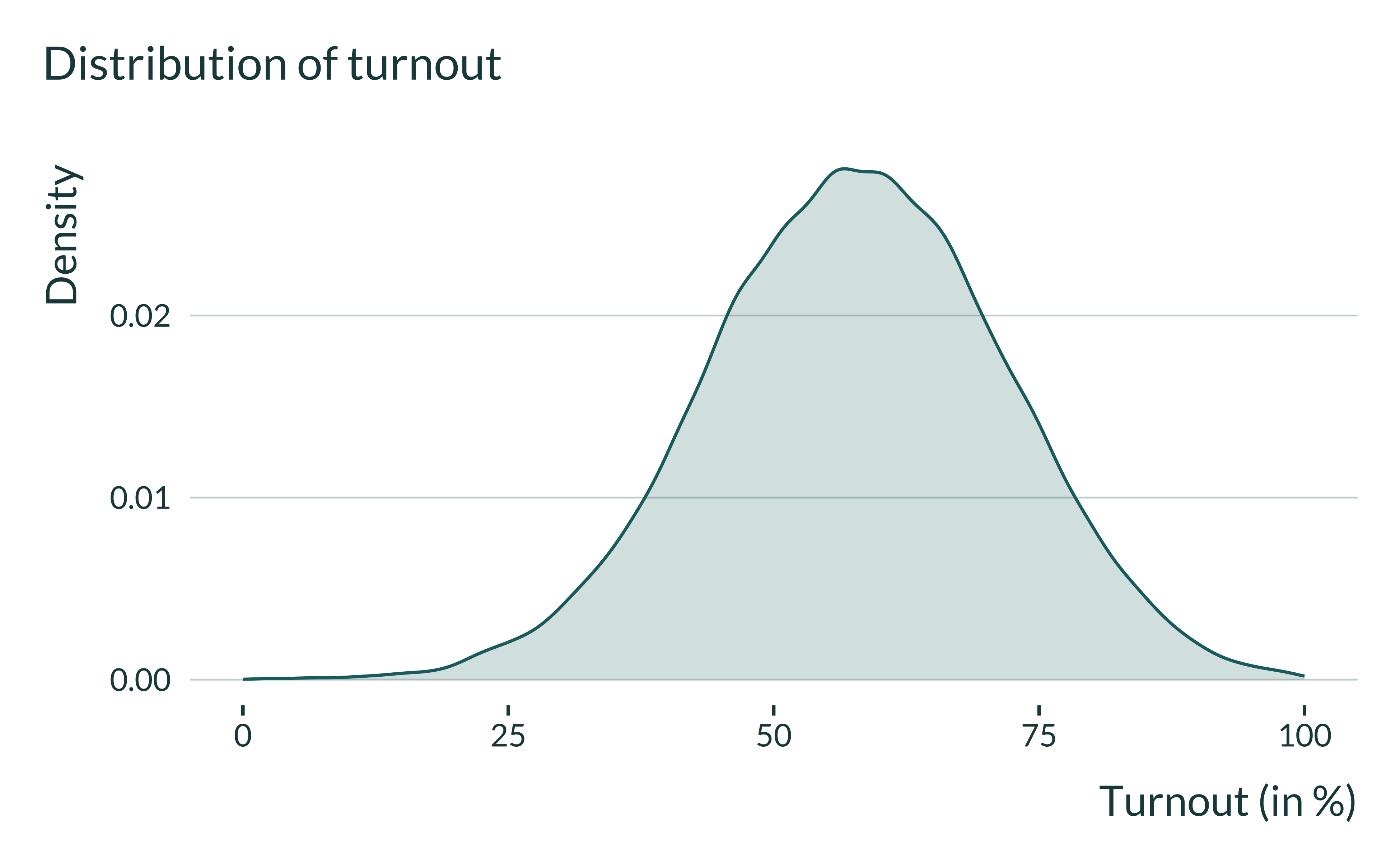

Exploring the distribution of the data

I just quickly explore the distribution of the data for a baseline set of parameters. For this, I consider a mid-range value for IV strength (-0.5).

Show the code used to generate the graph

ex_data_iv <- baseline_param_iv |>

pmap(generate_data_iv) |>

list_rbind()

ex_data_iv |>

ggplot(aes(x = turnout)) +

geom_density() +

labs(

title = "Distribution of turnout",

x = "Turnout (in %)",

y = "Density"

) +

xlim(c(0,100))

Show the code used to generate the graph

I also check the standard deviation and means of the variables and at the same time verify that they do not do not change when we vary \(\pi_1\). They are consistent with what we wanted:

Show the code used to generate the table

vect_pi_1 <- c(seq(0.1, 1, 0.1))

param_iv <- baseline_param_iv |>

select(-pi_1) |>

crossing(vect_pi_1) |>

rename(pi_1 = vect_pi_1)

gen_with_param <- function(...) {

generate_data_iv(...) |>

mutate(pi_1 = list(...)$pi_1)

}

ex_data_iv <- pmap(param_iv, gen_with_param) |>

list_rbind()

ex_data_mean <- ex_data_iv |>

group_by(pi_1) |>

summarise(across(.cols = c(share, turnout, rain), mean)) |>

mutate(stat = "mean")

ex_data_sd <- ex_data_iv |>

group_by(pi_1) |>

summarise(across(.cols = c(share, turnout, rain), sd)) |>

mutate(stat = "sd")

ex_data_mean |>

rbind(ex_data_sd) |>

pivot_wider(names_from = stat, values_from = c(share, turnout, rain)) |>

kable()| pi_1 | share_mean | share_sd | turnout_mean | turnout_sd | rain_mean | rain_sd |

|---|---|---|---|---|---|---|

| 0.1 | 48.04941 | 14.28623 | 59.27723 | 14.01282 | 2.320063 | 6.574221 |

| 0.2 | 48.13388 | 14.15855 | 59.48296 | 14.05485 | 2.367790 | 6.429612 |

| 0.3 | 48.09473 | 14.22863 | 59.73053 | 13.96563 | 2.281051 | 6.138917 |

| 0.4 | 47.88660 | 14.27701 | 59.91820 | 14.01559 | 2.320802 | 6.488280 |

| 0.5 | 47.98173 | 14.14524 | 60.14044 | 13.92176 | 2.304321 | 6.308877 |

| 0.6 | 47.71045 | 14.19988 | 60.49100 | 14.00489 | 2.375658 | 6.579245 |

| 0.7 | 48.01123 | 14.15247 | 60.56042 | 13.87831 | 2.304649 | 6.445715 |

| 0.8 | 47.81367 | 14.23189 | 60.84392 | 13.94361 | 2.322503 | 6.554110 |

| 0.9 | 47.62748 | 14.09742 | 61.25774 | 13.97077 | 2.309919 | 6.503217 |

| 1.0 | 47.62345 | 14.21288 | 61.50701 | 13.96111 | 2.384839 | 6.708181 |

Estimation

After generating the data, we can run an estimation. The goal is to compare the IV and the OLS for different IV strength values. Hence, I estimate both an IV and an OLS and return both set of outcomes of interest (point estimate, p-value, standard error and f-stat of the first stage).

estimate_iv <- function(data) {

# reg_iv <- AER::ivreg(data = data, formula = share ~ turnout | rain)

reg_iv <- feols(data = data, fml = share ~ 1 | 0 | turnout ~ rain)

fstat_iv <- fitstat(reg_iv, "ivf")$`ivf1::turnout`$stat

reg_iv <- reg_iv |>

broom::tidy() |>

mutate(model = "IV", fstat = fstat_iv)

reg_OLS <-

feols(data = data, fml = share ~ turnout) |>

broom::tidy() |>

mutate(model = "OLS", fstat = NA)

reg <- reg_iv |>

rbind(reg_OLS) |>

filter(term %in% c("turnout", "fit_turnout")) |>

rename(p_value = p.value, se = std.error) |>

select(estimate, p_value, se, fstat, model)

return(reg)

}One simulation

We can now run a simulation, combining generate_data_iv and estimate_iv. To do so I create the function compute_sim_iv. This simple function takes as input the various parameters. It returns a table with the estimate of the treatment, its p-value and standard error, the F-statistic for the IV, the true effect, the IV strength and the intensity of the OVB considered (delta). Note that for now, we do not store the values of the other parameters since we consider them fixed over the study.

The output of one simulation, for baseline parameters values is:

Show the code used to generate the table

pmap(baseline_param_iv, compute_sim_iv) |>

list_rbind() |>

kable()| estimate | p_value | se | fstat | model | pi_1 | delta | param_rain | true_effect |

|---|---|---|---|---|---|---|---|---|

| 0.1048483 | 0.8588483 | 0.5895587 | 3.196156 | IV | -0.05 | -13.4 | 0.13, 18.00 | -0.2 |

| -0.2804462 | 0.0000000 | 0.0056640 | NA | OLS | -0.05 | -13.4 | 0.13, 18.00 | -0.2 |

All simulations

I then run the simulations for different sets of parameters by mapping the compute_sim_iv function on each set of parameters. I thus create a table with all the values of the parameters we want to test, param_iv. Note that in this table each set of parameters appears n_iter times as we want to run the analysis \(n_{iter}\) times for each set of parameters.

Finally, I run all the simulations by looping the compute_sim_iv function on the set of parameters param_iv.

future::plan(multisession, workers = availableCores() - 1)

sim_iv <- future_pmap(param_iv, compute_sim_iv, .progress = TRUE) |>

list_rbind()

beepr::beep()

saveRDS(sim_iv, here("Outputs/sim_iv.RDS"))Analysis of the results

Quick exploration

First, I quickly explore the results.

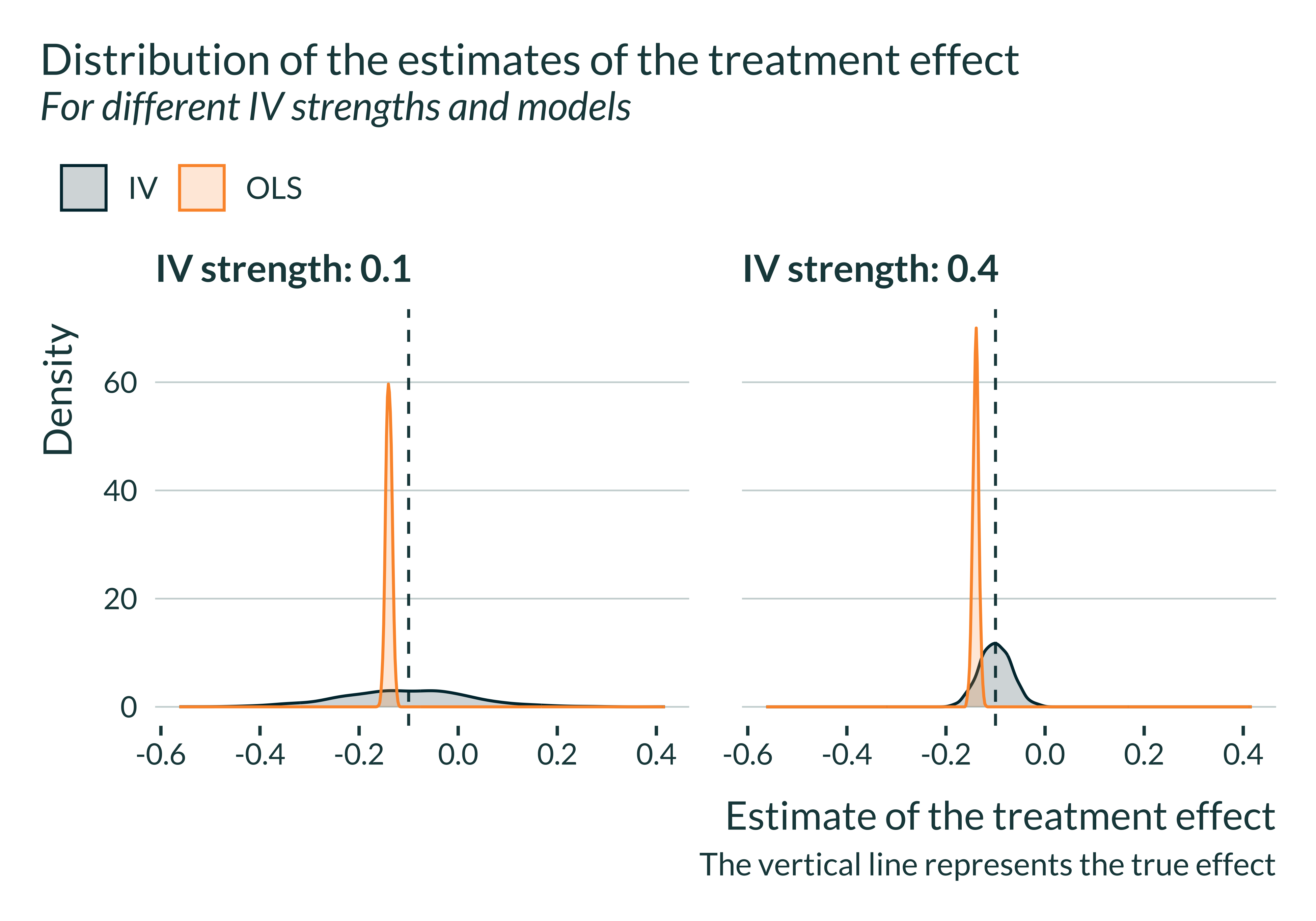

Show code

sim_iv <- readRDS(here("Outputs/sim_iv.RDS"))

sim_iv |>

filter(between(estimate, -1, 0.5)) |>

# filter(delta == sample(vect_delta, 1)) |>

filter(pi_1 %in% c(0.04, 0.2, 0.14)) |>

mutate(iv_strength = str_c("IV strength: ", pi_1)) |>

ggplot(aes(x = estimate, fill = model, color = model)) +

geom_vline(xintercept = unique(sim_iv$true_effect)) +

geom_density() +

facet_wrap(~ iv_strength) +

labs(

title = "Distribution of the estimates of the treatment effect",

subtitle = "For different IV strengths and models",

color = "",

fill = "",

x = "Estimate of the treatment effect",

y = "Density",

caption = "The vertical line represents the true effect"

) +

scale_mediocre_d()

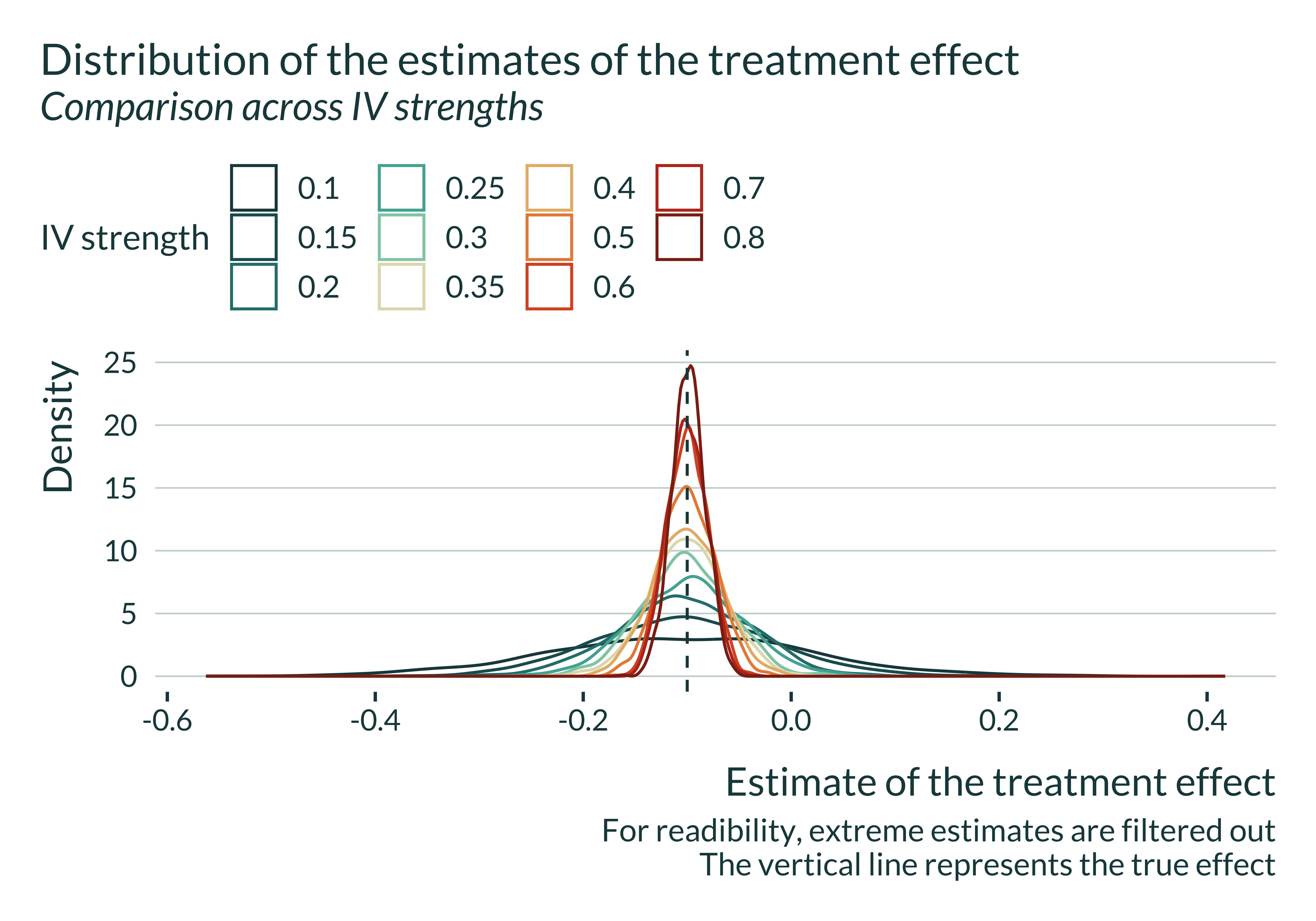

Show code

sim_iv |>

filter(between(estimate, -1.2, 1)) |>

filter(model == "IV") |>

ggplot() +

geom_density(aes(

x = estimate,

color = as.factor(pi_1)),

alpha = 0

) +

geom_vline(xintercept = unique(sim_iv$true_effect)) +

labs(

title = "Distribution of the estimates of the treatment effect",

subtitle = "Comparison across IV strengths",

color = "IV strength",

fill = "IV strength",

x = "Estimate of the treatment effect",

y = "Density",

caption = "For readibility, extreme estimates are filtered out

The vertical line represents the true effect"

)

Show code

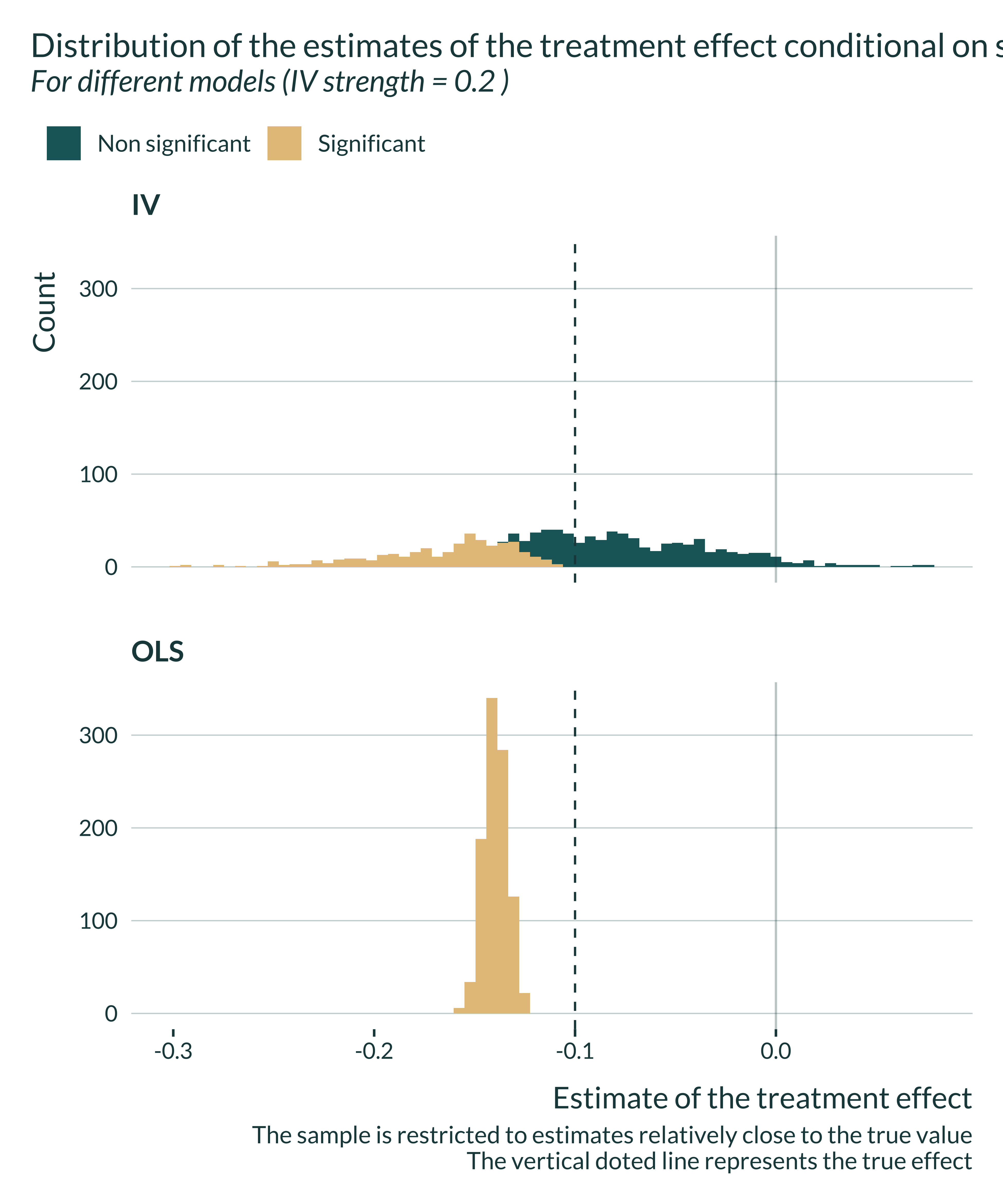

data_one_sim_iv <- sim_iv |>

filter(between(estimate, -0.5, 0.2)) |>

filter(pi_1 == 0.1) |>

mutate(significant = ifelse(p_value < 0.05, "Significant", "Non significant"))

data_one_sim_iv |>

ggplot(aes(x = estimate, fill = significant)) +

geom_histogram(bins = 70) +

geom_vline(xintercept = unique(sim_iv$true_effect)) +

geom_vline(xintercept = 0, linetype = "solid", alpha = 0.3) +

facet_wrap(~ model, nrow = 3) +

theme_mediocre(pal = "coty") +

labs(

title = "Distribution of the estimates of the treatment effect conditional on significativity",

subtitle = paste(

"For different models (IV strength =",

unique(data_one_sim_iv$pi_1), ")"

),

x = "Estimate of the treatment effect",

y = "Count",

fill = "",

caption = "The sample is restricted to estimates relatively close to the true value

The vertical doted line represents the true effect"

)

The OLS is always biased and that the IV is never biased. However, for limited IV strengths, the distribution of the estimates flattens. The smaller the IV strength, the most like it is to get an estimate away from the true value, even though the expected value remains equal to the true effect size.

Computing bias and exaggeration ratios

We want to compare \(\mathbb{E}\left[ \left| \frac{\widehat{\beta_{IV}}}{\beta_1}\right|\right]\) and \(\mathbb{E}\left[ \left| \frac{\widehat{\beta_{IV}}}{\beta_1} \right| | \text{signif} \right]\). The first term represents the bias and the second term represents the exaggeration ratio.

To do so, I use the function summmarise_sim defined in the functions.R file.

Graph

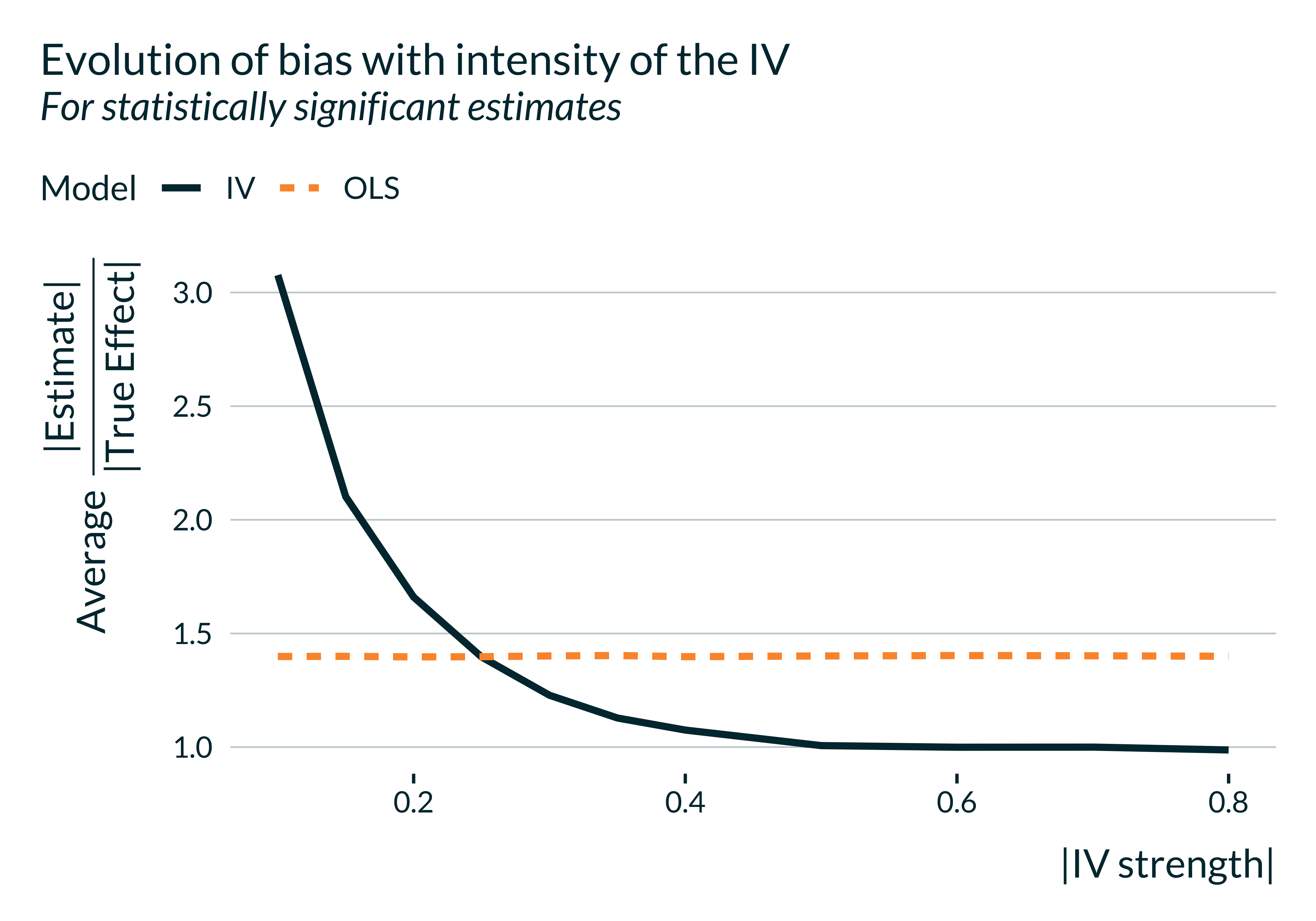

To analyze the results, I build a unique and simple graph:

Show the code used to generate the graph

main_graph_iv <- summary_sim_iv |>

ggplot(aes(x = abs(pi_1), y = type_m, color = model)) +

geom_line(size = 1.2, aes(linetype = model)) +

# geom_point(size = 3) +

labs(

x = "|IV strength|",

y = expression(paste("Average ", frac("|Estimate|", "|True Effect|"))),

color = "Model",

linetype = "Model",

title = "Evolution of bias with intensity of the IV",

subtitle = "For statistically significant estimates"

) +

scale_y_continuous(breaks = scales::pretty_breaks(n = 4)) +

scale_mediocre_d()

main_graph_iv

If IV strength is low, on average, statistically significant estimates overestimate the true effect. If the IV strength is too low, it might even be the case that the benefit of the IV is overturned by the exaggeration issue. The IV yields an unbiased estimate and enables to get rid of the OVB but such statistically significant estimates fall, on average, even further away from the true effect.

Of course, if one considers all estimates, as the IV is unbiased, this issue does not arise.

Distribution of the estimates

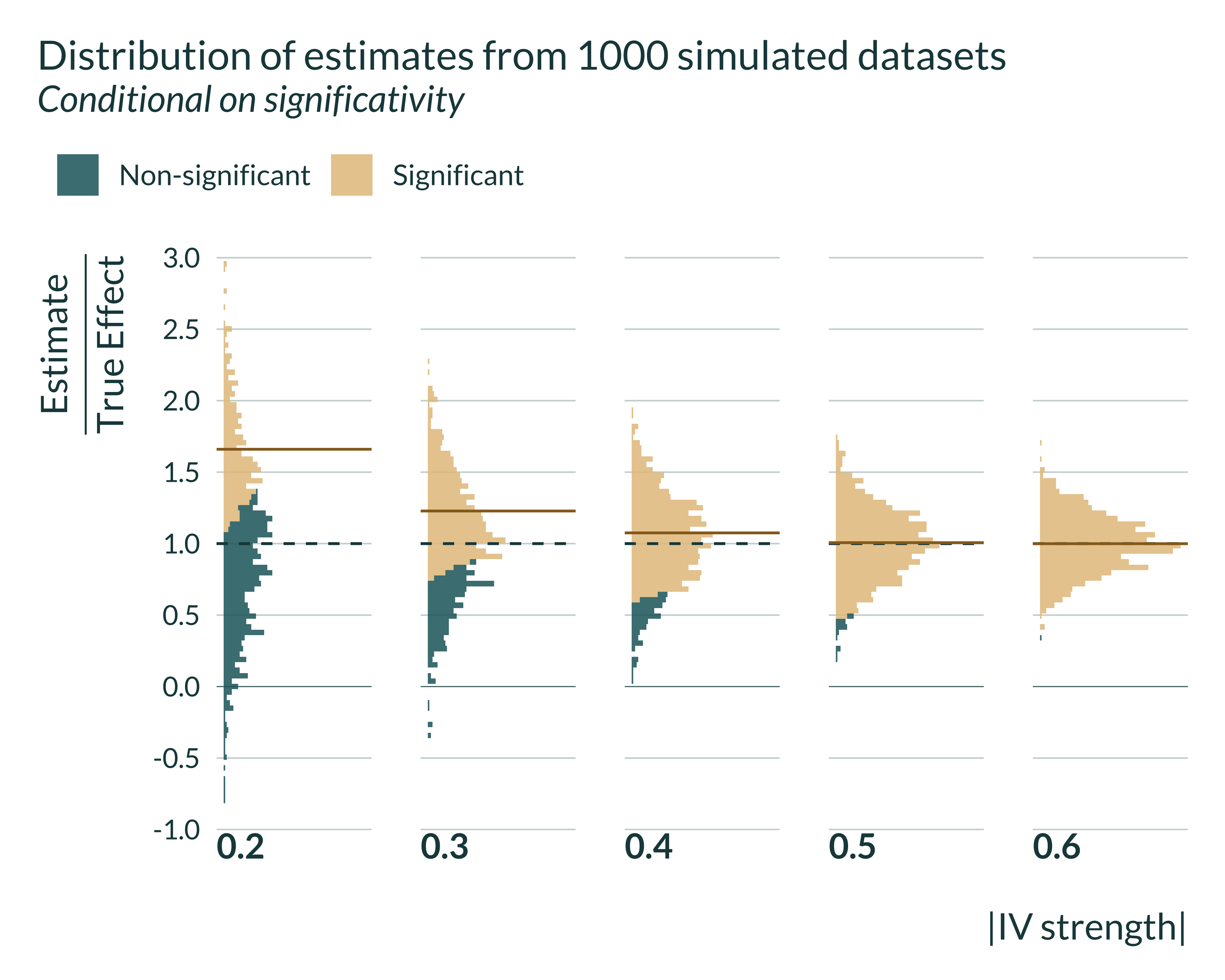

I then graph the distribution of estimates conditional on significativity. It represents the same phenomenon but with additional information.

Show the code used to generate the graph

set_mediocre_all(pal = "coty")

sim_iv |>

filter(model %in% c("IV")) |>

mutate(

signif = ifelse(p_value < 0.05, "Significant", "Non-significant"),

ratio_exagg = estimate/true_effect

) |>

group_by(pi_1, model) |>

mutate(

mean_signif = mean(ifelse(p_value < 0.05, ratio_exagg, NA), na.rm = TRUE),

mean_all = mean(ratio_exagg, na.rm = TRUE)

) |>

ungroup() |>

filter(as_factor(pi_1) %in% seq(0.02, 0.16, 0.02)) |>

ggplot(aes(x = ratio_exagg, fill = "All Estimates")) +

facet_grid(~ pi_1, switch = "x") +

geom_vline(xintercept = 1) +

geom_vline(xintercept = 0, linetype = "solid", linewidth = 0.12) +

scale_x_continuous(breaks = scales::pretty_breaks(n = 6)) +

coord_flip() +

scale_y_continuous(breaks = NULL) +

labs(

y = "|IV strength|",

x = expression(paste(frac("Estimate", "True Effect"))),

fill = "",

title = "Distribution of estimates from 1000 simulated datasets",

subtitle = "Conditional on significativity",

# caption =

# "The green dashed line represents the result aimed for

# "The brown solid line represents the average of significant estimates"

) +

geom_histogram(bins = 100, alpha = 0.85, aes(fill = signif)) +

geom_vline(xintercept = 1) +

geom_vline(

aes(xintercept = mean_signif),

color = "#976B21",

linetype = "solid",

size = 0.5

)

Further checks

Magnitude of exaggeration

To be able to determine where an actual setting could fall on the main graph, let’s discuss again what are realistic values for the strength of the IV in this setting. The exaggeration ratios we found in my simulations are as follows:

| IV strength | Exaggeration Ratio | Median SNR |

|---|---|---|

| 0.03 | 3.83 | 0.69 |

| 0.04 | 3.18 | 0.77 |

| 0.05 | 2.86 | 0.91 |

| 0.06 | 2.49 | 1.05 |

| 0.07 | 2.14 | 1.14 |

| 0.08 | 1.86 | 1.29 |

| 0.09 | 1.74 | 1.55 |

| 0.10 | 1.57 | 1.66 |

| 0.11 | 1.48 | 1.83 |

| 0.12 | 1.39 | 1.96 |

| 0.16 | 1.16 | 2.64 |

| 0.20 | 1.06 | 3.24 |

| 0.24 | 1.01 | 3.89 |

| 0.28 | 1.00 | 4.60 |

As discussed above, a typical magnitude of the first stage effect (IV strength) is around -0.05. That would be associated with an exaggeration ratio of about 2.9.

Representativeness of the estimation

I calibrated the simulations to emulate a typical study from this literature. To further check that the results are realistic, I compare the average Signal-to-Noise Ratio (SNR) of the simulations to the range of \(t\)-stats of an existing study. In Hansford and Gomez (2010) (Table 1, column 2), the \(t\)-stat is about 1.7. However, in this specification, there are interaction terms for turnout. I replicate the results dropping the estimation terms. In that instance, the \(t\)-stats is about 3.9. While they do not compute the same 2SLS, Fujiwara, Meng, and Vogl (2016) estimate a reduced form estimate of the impact of rain on republican vote share; they get a t-stat of 1.7. (table A3).

For SNRs of the order of magnitude of the \(t\)-stats observed in the literature, exaggeration can be substantial.

Code to replicate Hansford and Gomez

# I retrieve data for Hansford and Gomez (2010) from here:

#https://myweb.fsu.edu/bgomez/research.html

library(readr)

hansford <- read_csv(here("inputs", "IV_vote", "HansfordGomez_data.csv"))

#replication

feols(

DemVoteShare2 ~ DemVoteShare2_3MA + Yr52 + Yr56 + Yr60 + Yr64 + Yr68 +

Yr72 + Yr76 + Yr80 + Yr84 + Yr88 + Yr92 + Yr96 + Yr2000 |

FIPS_County |

Turnout + GOPIT + TO_DVS23MA ~ DNormPrcp_KRIG + RainGOPI + Rain_DVS23MA,

data = hansford,

vcov = "hetero"

)

#removing interactions

feols(

DemVoteShare2 ~ DemVoteShare2_3MA + Yr52 + Yr56 + Yr60 + Yr64 + Yr68 +

Yr72 + Yr76 + Yr80 + Yr84 + Yr88 + Yr92 + Yr96 + Yr2000 |

FIPS_County |

Turnout ~ DNormPrcp_KRIG,

data = hansford,

vcov = "hetero"

)F-statistic analysis

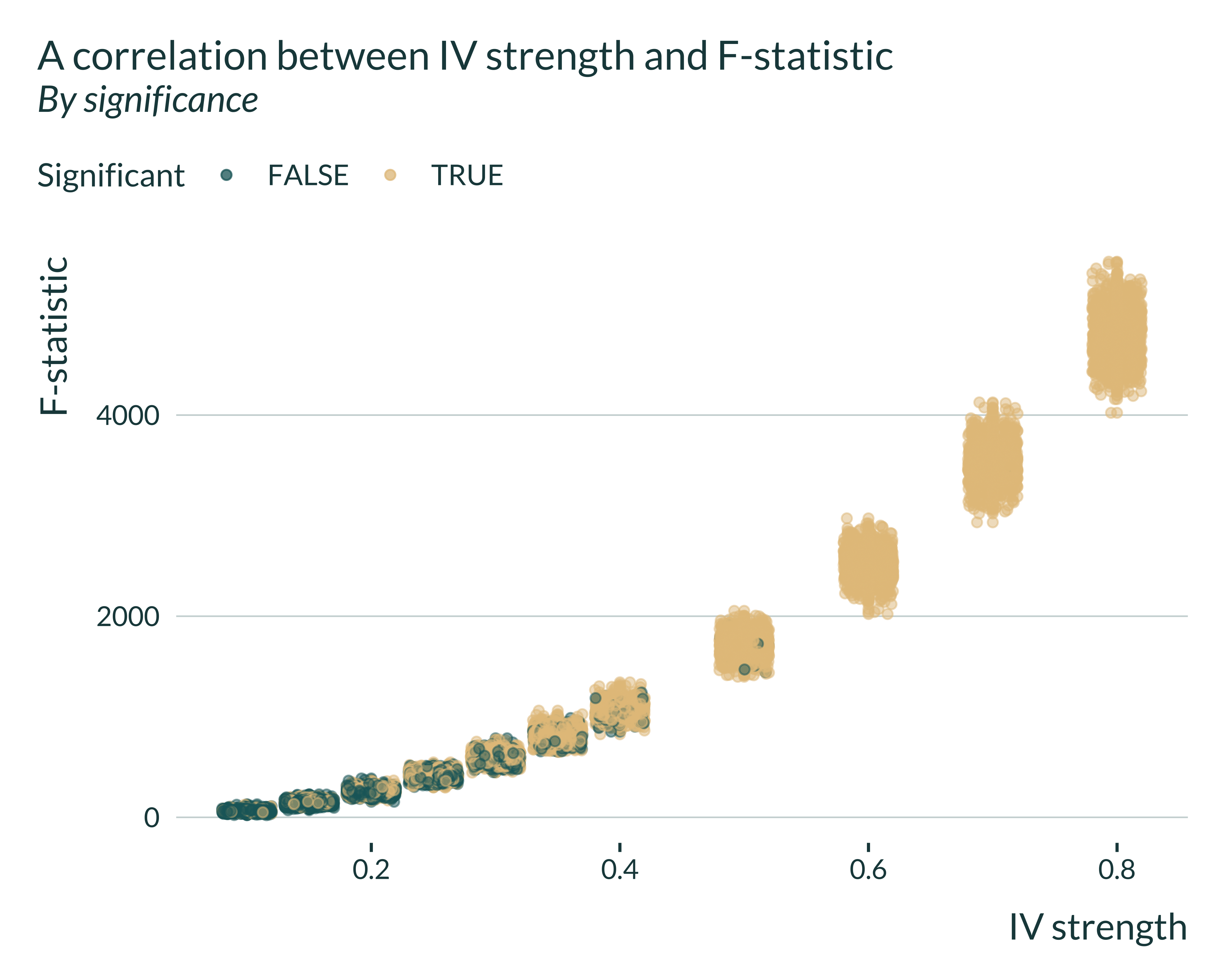

I then run some exploratory analysis to study the link between exaggeration and F-stat (under construction).

Show the code used to generate the graph

sim_iv |>

filter(model == "IV") |>

mutate(signif = (p_value <= 0.05)) |>

ggplot(aes(x = pi_1, y = fstat, color = signif)) +

geom_point(alpha = 0.5) +

geom_jitter(alpha = 0.5) +

labs(

title = "A correlation between IV strength and F-statistic",

subtitle = "By significance",

x = "IV strength",

y = "F-statistic",

color = "Significant"

)

Show the code used to generate the graph

# ylim(c(0, 40))

# lm(data = sim_iv, fstat ~ pi_1) |>

# summary() %>%

# .$adj.r.squared

# sim_iv |>

# mutate(significant = (p_value <= 0.05)) |>

# filter(model == "IV") |>

# ggplot() +

# geom_density_ridges(aes(x = fstat, y = factor(pi_1), fill = significant, color = significant), alpha = 0.6)+

# coord_flip() +

# xlim(c(0, 50)) +

# labs(

# title = "F-statistics larger than 10, even for small IV strength",

# subtitle = "Distribution of F-statistics by IV strength and significance",

# x = "F-statistic",

# y = "IV strength",

# fill = "Significant",

# color = "Significant"

# )

# sim_iv |>

# filter(model == "IV") |>

# mutate(

# significant = (p_value <= 0.05),

# bias = abs((estimate - true_effect)/true_effect)

# ) |>

# filter(fstat > 10) |>

# ggplot(aes(x = pi_1, y = fstat, color = bias)) +

# geom_point(alpha = 0.5) +

# geom_jitter(alpha = 0.5) +

# labs(

# title = "A correlation between IV strength and F-statistic",

# subtitle = "By significance",

# x = "IV strength",

# y = "F-statistic"

# # color = "Significant"

# )

# sim_iv |>

# filter(model == "IV") |>

# mutate(

# significant = (p_value <= 0.05)

# ) |>

# group_by(pi_1) |>

# summarise(

# mean_fstat = mean(fstat),

# type_m = median(ifelse(significant, abs(estimate/true_effect), NA), na.rm = TRUE)

# ) |>

# ggplot(aes(x = pi_1, y = mean_fstat, color = type_m)) +

# geom_point() +

# # geom_jitter(alpha = 0.5) +

# labs(

# title = "A correlation between IV strength and F-statistic",

# subtitle = "By significance",

# x = "IV strength",

# y = "F-statistic"

# # color = "Significant"

# ) +

# ylim(c(0,20))Unsurprisingly, there is a clear positive correlation between what we call IV strength and the F-statistic. I then investigate the link between exaggeration ratios and F-statistics.

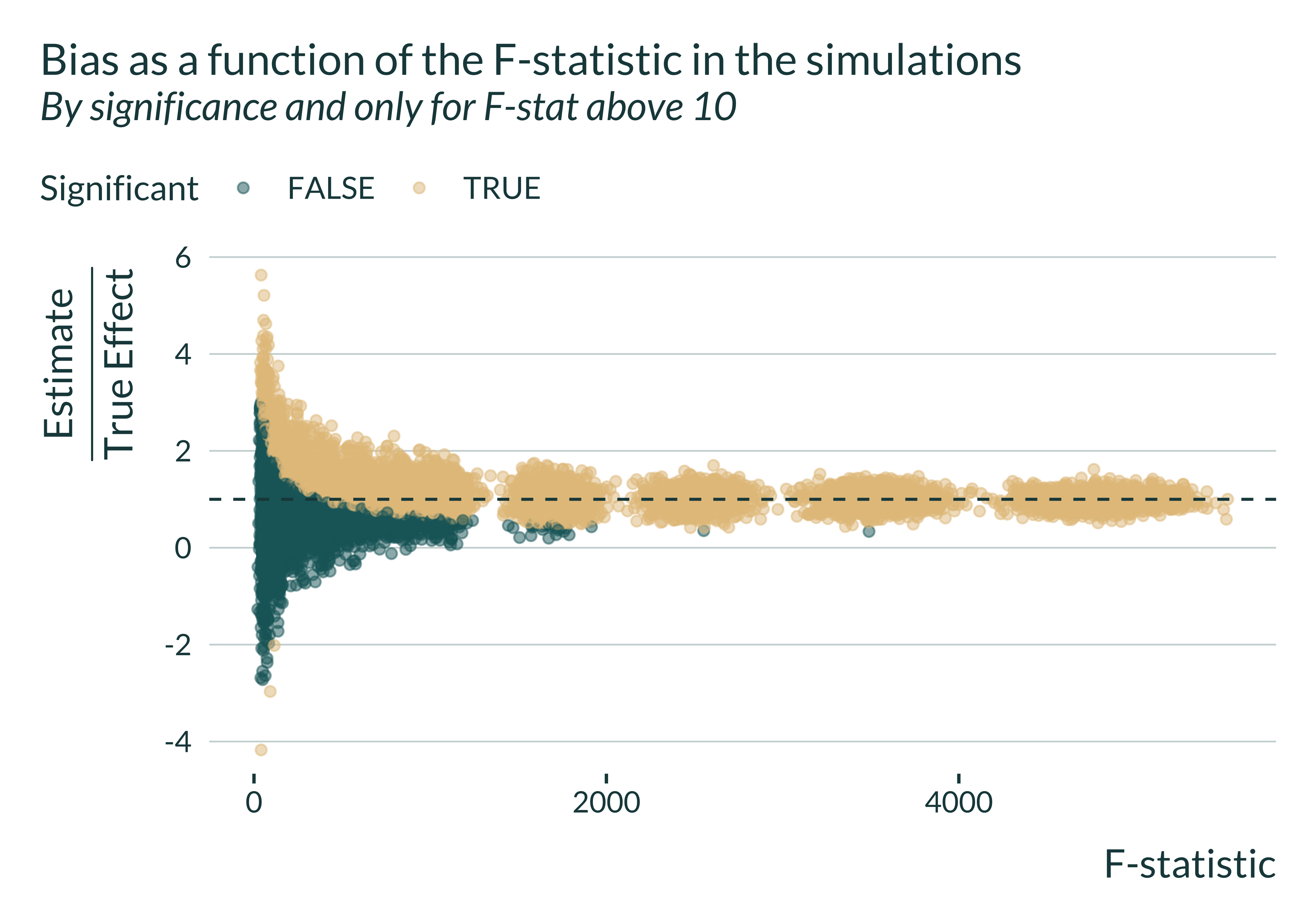

Show code

sim_iv |>

filter(model == "IV") |>

mutate(significant = (p_value <= 0.05)) |>

mutate(bias = estimate/true_effect) |>

filter(fstat > 10) |>

# pull(bias) |>mean(., na.rm = TRUE)

# filter(abs(bias) < 10) |>

ggplot(aes(x = fstat, y = bias, color = significant)) +

geom_point(alpha = 0.5) +

geom_hline(yintercept = 1) +

labs(

title = "Bias as a function of the F-statistic in the simulations",

subtitle = "By significance and only for F-stat above 10",

x = "F-statistic",

y = expression(paste(frac("Estimate", "True Effect"))),

color = "Significant"

)

We notice that, even when the F-statistic is greater than the usual but arbitrary threshold of 10, statistically significant estimates may, on average overestimate the true effect.

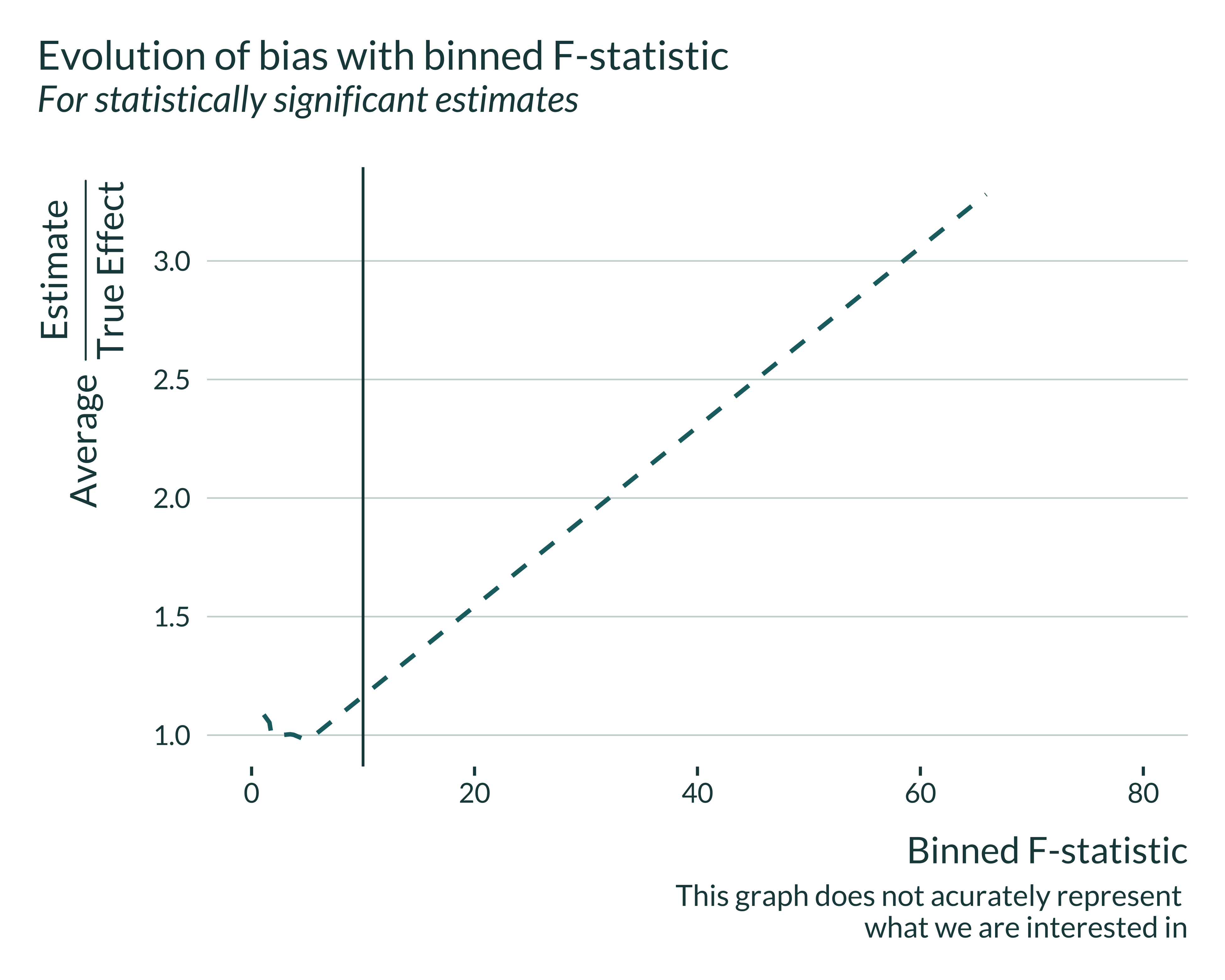

We cannot compute directly the bias of interest against the F-statistic because the F-statistic is not a parameter of the simulations and we do not control them, only the IV strength. To overcome this, I compute the median power by binned F-statistic. However, this is not correct as we end up comparing and pulling together simulations with different parameter values. I still display the graph, keeping this limitation in mind:

Show code

sim_iv |>

filter(model == "IV") |>

mutate(

significant = (p_value <= 0.05),

bin_fstat = cut_number(fstat, n = 20) |>

paste() |>

str_extract("(?<=,)(\\d|\\.)+") |>

as.numeric()

) |>

group_by(delta, bin_fstat) |>

summarise(

power = mean(significant, na.rm = TRUE)*100,

type_m = mean(ifelse(significant, abs(estimate - true_effect), NA), na.rm = TRUE),

bias_signif = mean(ifelse(significant, estimate/true_effect, NA), na.rm = TRUE),

bias_all = mean(estimate/true_effect, na.rm = TRUE),

bias_all_median = median(estimate/true_effect, na.rm = TRUE),

median_fstat = mean(fstat, na.rm = TRUE),

.groups = "drop"

) |>

ungroup() |>

ggplot(aes(x = bin_fstat, y = bias_signif)) +

geom_line(linetype = "dashed") +

geom_vline(xintercept = 10, linetype ="solid") +

xlim(c(0, 80)) +

labs(

x = "Binned F-statistic",

y = expression(paste("Average ", frac("Estimate", "True Effect"))),

color = "Model",

title = "Evolution of bias with binned F-statistic",

subtitle = "For statistically significant estimates",

caption = "Note that this graph does not acurately represent

what we are interested in"

)